Inflation can be Many Things to Many People

05/15/07

The Dow Jones Industrial Index closed yesterday at yet another record high, while the rest of the market suffered a very ugly reversal. The S&P; 500 had jumped in the morning at the release of the Consumer Price Index which showed moderating inflation for the core index. In the afternoon, the National Association of Home Builders' monthly Housing Market Index fell back to a 16-year low, falling to 30 from 33 in April and matching last September's low, which was the lowest since February 1991. This was more than even the most bullish trader could bear and investors decided that it was prudent to take some profits. While the Dow Jones was able to close the day in positive territory again, the Russel 2000, which measures the performance of stocks with a small market capitalization, ended by over 1% in the red. Interestingly enough, even bonds sold off, although inflation numbers contained no surprises and overall inflation seemed to moderate.

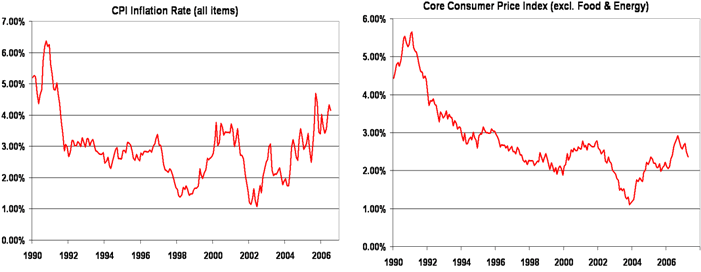

You can see that the left chart is staying in a trend channel that point steeply upwards. Rising energy and food prices keep the year over year increase well above the Federal Reserves target of 2%. Core inflation (right chart), which includes the falling cost of housing in the U.S., has mellowed to a 2.3% year-over-year rate.

Liz Rappaport said it very nicely yesterday: "The divergence in the stock market highlights the U.S. economy's delinking from, and dependence on, other economies around the globe. The Russell represents unbridled growth in the U.S., while the large-cap Dow represents unbridled growth in the world. With the U.S. well into its midcycle slowdown, the global growth bet is safer. ... The Russell-Dow divergence is also similar to the divergence between headline and core inflation, and a reminder of the same global dynamics. Headline consumer inflation, which includes the costs of energy and food, is running at a 5.6% year-over-year rate, rising amid global demand for energy and basic materials. Core inflation, which includes the falling cost of housing in the U.S., has mellowed to a 2.3% year-over-year rate." For the first time, the U.S. economy no longer leads but follows. This is significant and will probably become even more pronounced. The growth rate of virtually any emerging economy is probably three times as high as our domestic economic growth. This means that the big capitalization stocks in the Dow Jones Industrials average, which are benefiting more from international than from domestic growth will continue to outperform their smaller and more domestic oriented brethren in the Russell 2000 index. For the past 5 years, small cap stocks in the Russell 2000 have been outperforming the large caps in this country and in most other international exchanges until May last year. Then a hiccup occurred and from that point on, large caps started to outperform.

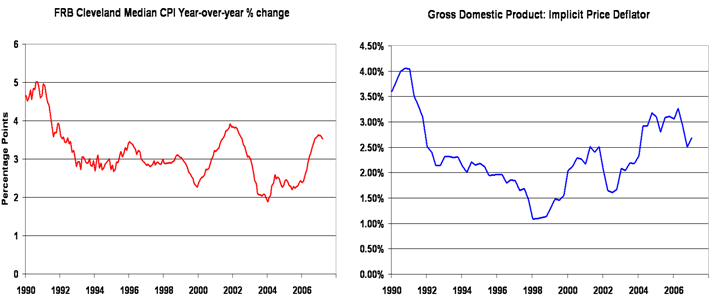

Inflation is an important variable for monetary policy at every central bank. Measuring the general level of prices is difficult, as nonmonetary events can, at least temporarily, distort reported inflation statistics, such as the Consumer Price Index (CPI). During periods of bad weather, for example, food prices may rise to reflect decreased supply, producing transitory increases in the CPI. But since these prices do not constitute monetary inflation, monetary policymakers may want to avoid including them in their decision-making. One commonly used technique for measuring underlying or core inflation is to exclude certain prices in the computation of the index, based on the assumption that these prices are the ones with "high-noise" components. This is the rationale behind the commonly reported CPI excluding food and energy data. However, economists Michael Bryan and Stephen Cecchetti have found a measure that forecasts inflation better than either the CPI excluding food and energy or the all items CPI: a weighted median of the CPI. The weighted median CPI is easy to calculate and has a higher correlation with past money growth than other inflation measures, resulting in improved forecasts of future inflation, according to the Cleveland Federal Reserve. You can see the result in the left chart below: 3.52%

The CPI in al its variations is relying on baskets of goods and services, which measure things like homeowners equivalent rent and such. The concepts may be valid and well thought out, the fact is however, that a basket measures what is put in. If one wanted to measure what everybody is paying in real life, one can observe real world price behavior by implication. The Implicit Price Deflator is always released together with the Gross Domestic Products estimates. The math is simple: Current dollar GDP divided by constant dollar GDP. This ratio is used to account for the effects of inflation, by reflecting the change in the prices of the bundle of goods that make up the GDP as well as the changes to the bundle itself. You can see the effect in the right chart above. 2.69%

So now we have an entire spectrum of inflation measurements ranging from 2.3% to 5.6%. I guess inflation is more a feeling than a measured number. When people complain about inflation, they usually complain about the prices that are rising and they tend to forget about the ones that are going down. In this sense, China is playing a vital role again. By becoming the workshop of the world, China has pushed down the prices of all mass-produced manufactured goods. Some things, however, can not be traded and therefore are less exposed to competition. Healthcare, housing and education have continued to dramatically rise in price. Some things can be traded but are not produced in China: Oil and raw materials. Both of those areas feel the brunt of inflation and those areas are what people mean when they complain about inflation.

And then there are the areas of luxury items and services for the wealthy which have seen the most dramatic price increases of them all. Just ask anybody who had to buy a luxury yacht, had to "do some plastic surgery" or had to send his kids to a private school: "It has never been so expensive to be rich."

Hermann Vohs